- Vincent Spotlight

- Posts

- Investing in Real Estate Debt

Investing in Real Estate Debt

Adam Katz

June 26, 2024

Investing in Real Estate Debt

Investment portfolios should consist of assets that offer value appreciation and assets that offer yield. To achieve that mix, modern investors are looking beyond public debt and equities and into alternative assets. Americans ranked real estate as the #1 long-term investment over the past decade, and it’s usually considered the most popular alternative asset.

Investing in real estate takes many forms, such as rental property, shares of REITs, and real estate syndications. Among the different ways of investing in real estate, investors are increasingly considering real estate debt as a new way to diversify. The recent advent of fractionalization makes it easier than ever to access this part of the capital stack in the asset class, though there are still limited opportunities for non-accredited investors.

Groundfloor allows non-accredited investors to invest fractionally in real estate debt with low minimums.

What is Real Estate Debt?

Debt financing is at the core of the real estate industry, and investing in it is often closer to a private credit deal than a traditional real estate deal. Typically, borrowers need money to purchase or renovate a property, with the property itself serving as collateral. They agree to repay the loan amount at a specified interest rate over a specified period of time to the lender, usually a bank or a private entity, but can also be an individual.

The Capital Stack (RealtySlices)

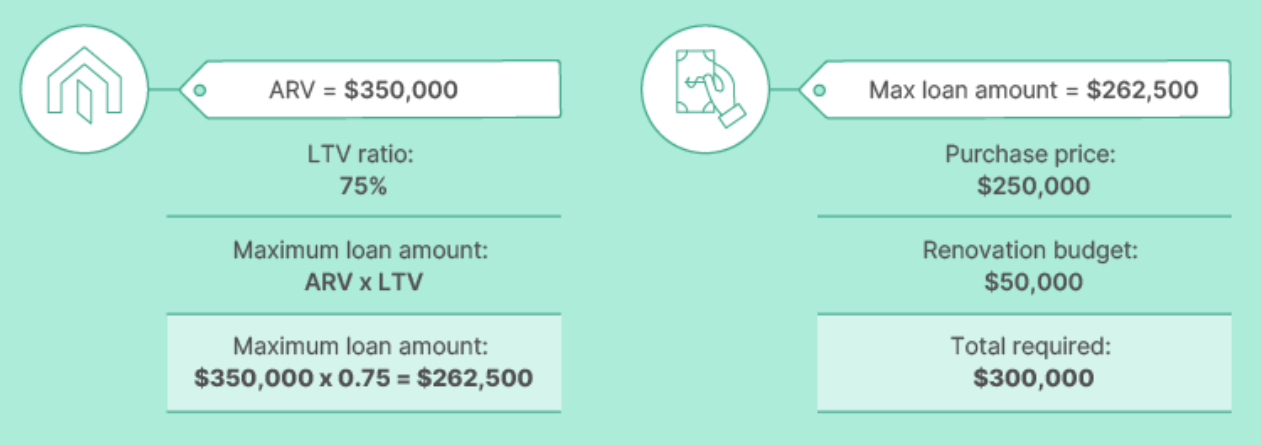

There are many types of real estate debt, from standard residential and commercial mortgages, to construction loans, renovation loans, land loans, with a myriad of different structures and terms. Often they are packaged into mortgage-backed securities, but those are generally only available to institutional investors. It is always important to understand the specific terms of any deal, including the interest rate, the repayment timeline, the position of the loan, the loan-to-value ratio (LTV), and in the case of construction or renovation loans, the after-repair value (ARV) of a property.

Most people associate real estate investing with equity investing rather than debt investing. Equity investing involves collecting rental income, paying for property expenses, and capturing the reward of appreciation or the downside of falling property values. Debt investing is more straightforward and offers steadier returns with both a lower upside and lower downside.

How Should You Evaluate Real Estate Debt Opportunities?

To mitigate the risks associated with real estate debt, it is important to research each opportunity before investing. Here are some factors to consider:

Borrower

History of successful repayments and project completions

Experience in the real estate industry

Are they a full-time developer or rehabber?

Income

Current reserves

Credit Score

Property

Property value

After-repair value (ARV) - for construction and rehab loans

Loan-to-value ratio or Loan-to-ARV-ratio

Potential rental income and expenses

Location of the market and within the market

(Kiavi)

Loan

Terms of the loan - length and interest rate

Position of loan (senior debt v. junior debt)

Originator - history, reliability

Why Invest in Real Estate Debt?

While the high interest rate environment has recently had the greater real estate market in a holding pattern, it has provided a boost to debt investors in the form of higher yields. Debt can be a good way to diversify your portfolio while providing a passive income stream. Real estate debt is also usually secured by a real asset, limiting the downside risk compared to common private credit deals where a company can simply go bankrupt. Often, investing into real estate debt deals requires less capital than real estate equity deals and also offers greater liquidity, with investment terms as short as a month.

There are, of course, risks associated with real estate debt, as there would be in any investment. The borrower can default on the loan, which is mitigated if the loans are secured by property. However, property values can decline, and if a property is underwater - meaning the debt owed exceeds the property value - not all funds may be recovered even in the case of a foreclosure. In the case of construction or renovation loans, there is a risk that the project stalls or is never completed. Typically, the higher the promised return of a deal, the higher the implied risk.

Who is Groundfloor?

Groundfloor is an online platform and mobile app where everyday investors can access fractionalized real estate debt investment opportunities. Founded in 2013 by Brian Dally and Nick Bhargava (a regulatory expert who helped draft the 2012 JOBS Act that ushered in the crowdfunding era), Groundfloor has been named to the Forbes Fintech 50, the Deloitte Fast 500 three times and the Inc 5000 four times. It has more than 250,000 users who have collectively invested over $1.4 billion thus far. Groundfloor was the first company to be qualified by the SEC to offer real estate debt investments to both accredited and non-accredited investors.

Groundfloor is an originator that focuses on short-term, high-interest loans, lending funds to individuals and small businesses, helping them transform houses in neighborhoods across the country. They then fractionalize those loans, allowing people to invest as little as $1 into them.

Groundfloor has consistently delivered strong returns to its investors, with a rate of return consistently approaching 10%. Because Groundfloor makes its money on loan origination and servicing, investors keep the entirety of interest rate payments and are not charged any fees.

Historical Performance

What does Groundfloor offer to investors?

Groundfloor allows everyone, including non-accredited investors, to invest fractionally in real estate debt and has a number of offerings.

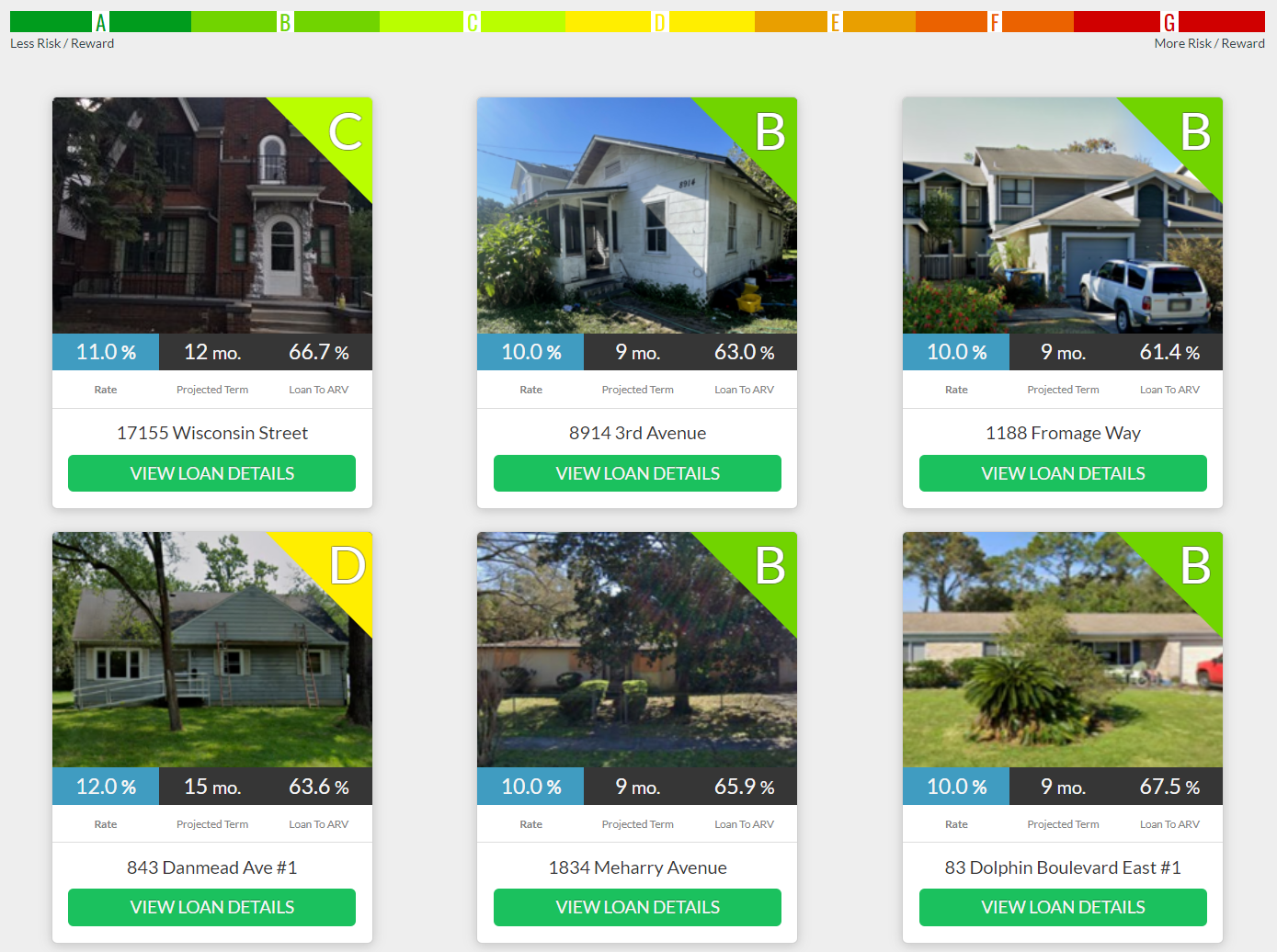

The first, Limited Recourse Obligations (LROs), are all SEC-qualified, first-position loans that are backed by an underlying real estate asset. They grade each loan on a scale from A (lowest potential risk and return) to G (highest potential risk and return), here is a detailed look at how they arrive at the grade and their lending guidelines.

Examples of LROs

Groundfloor Notes are secured debt offerings with a set date repayment term, making them ideal for people looking for a consistent and predictable source of passive income. Standard Notes have 30-day, 90-day or 12-month terms, while Rollover Notes have 30-day and 90-day terms. Rollover Notes allow investors to have their principal automatically reinvested at the end of a loan duration.

Groundfloor also works with an IRA custodian, Forge Trust, to offer self-directed IRAs, allowing investors the tax benefits of an IRA. Groundfloor is currently waiving all investor fees associated with IRAs through December 2024.

Auto-Investor

The most straightforward way to invest on Groundfloor is by using their Auto Investor product, where investors are automatically invested in every available loan (usually between 50-100 at any given time) on their platform at an even distribution. This approach minimizes risk by spreading it over enough loans so the overall portfolio can withstand any non-performing loans. Historically, this has produced consistent returns between 9-12%. And, as loans get repaid, the repayments will automatically be invested in new loans on the platform. As time goes on, the Auto Investor product enables an investor to build a diversified portfolio that produces consistent returns with lower risk.

Why Groundfloor?

For most people, investing fractionally or into a fund is going to be the only way to get access to real estate debt offerings -- very few individuals have the time or capital to originate loans themselves. The track record of the company you choose to invest in is of vital importance. Groundfloor has over a decade of delivering results to their investors. And the Auto Investor product means that you can let them do the work for you with the ability to fractionalize your investments down to $1.

For a very accessible, low minimum investment of $10, you can see stable returns with limited volatility and risk, and regular cash distributions. Short loan periods mean greater liquidity than most other real estate investments, and fractional ownership allows you to diversify your portfolio across hundreds of projects. Groundfloor’s mobile app is easy to use and allows you to track investments easily and makes sure you stay up-to-date on how they are performing.

How to Get Started?

The first step is to visit the Groundfloor website or download the Groundfloor mobile app, and then create your account. Then, connect your bank account and make your first investment with as little as $10. If you want to let Auto Investor do the rest, you can, or you can choose a more self-directed option to invest in the offerings you want.

Sign up for Groundfloor using the referral code “VINCENT” and invest at least $100, and you’ll get a $50 investment bonus to start building your portfolio.

Note: If you are an international investor, you are allowed to invest on the platform, but you have to email [email protected] to transfer in funds and begin investing, and the minimum initial investment is $5,000.

Invest in Groundfloor

Every two years, Groundfloor offers equity in the company in a crowdfunding raise. Be on the lookout for this opportunity, which should be available in the near future.